"/><stop offset="1" stop-color="rgb(3, 73, 122)"/></linearGradient><linearGradient id="qyqFJaVjA-1921182794-linear-gradient" x1="0" x2="1" y1="0.5558218829289385" y2="0.4441781170710614"><stop offset="0" stop-color="rgb(29, 170, 88)"/><stop offset="1" stop-color="rgb(0, 143, 203)"/></linearGradient><linearGradient id="KBptSRBQO-1921182794-linear-gradient" x1="0" x2="1" y1="0.5556785500517466" y2="0.44432144994825334"><stop offset="0" stop-color="rgb(29, 170, 88)"/><stop offset="1" stop-color="rgb(0, 143, 203)"/></linearGradient><linearGradient id="Kgw6PgukY-1921182794-linear-gradient" x1="0.2117440484028747" x2="0.7882559515971252" y1="1" y2="5.551115123125783e-17"><stop offset="0" stop-color="rgb(0, 143, 203)"/><stop offset="1" stop-color="rgb(255, 255, 255)"/></linearGradient></defs><g d="M 25.388 5.232 L 25.388 10.89 L 26.819 10.89 C 29.017 10.89 30.33 9.837 30.33 8.061 C 30.33 6.285 28.996 5.232 26.766 5.232 L 25.387 5.232 Z M 24 12.008 L 24 4.118 L 26.79 4.118 C 29.895 4.118 31.746 5.599 31.746 8.065 C 31.746 10.53 29.916 12.012 26.844 12.012 L 24 12.012 Z M 38.74 9.415 C 38.233 8.438 37.652 7.265 37.166 6.248 C 36.665 7.317 36.137 8.373 35.582 9.415 Z M 37.113 4 L 37.22 4 L 41.53 12.015 L 40.064 12.015 L 39.179 10.413 L 35.129 10.413 L 34.266 12.015 L 32.799 12.015 L 37.109 4 Z M 45.954 5.232 L 45.954 12.008 L 44.567 12.008 L 44.567 5.232 L 41.809 5.232 L 41.809 4.118 L 48.714 4.118 L 48.714 5.232 L 45.955 5.232 Z M 54.927 9.415 C 54.421 8.438 53.84 7.265 53.354 6.248 C 52.853 7.317 52.324 8.373 51.77 9.415 L 54.928 9.415 Z M 53.302 4 L 53.409 4 L 57.719 12.015 L 56.256 12.015 L 55.371 10.413 L 51.321 10.413 L 50.458 12.015 L 48.992 12.015 Z M 59.88 12.008 L 59.88 4.114 L 61.268 4.114 L 61.268 10.89 L 65.158 10.89 L 65.158 12.008 Z M 68.892 4.5 L 67.5 4.5 L 67.5 12.39 L 68.892 12.39 Z M 76.924 12.177 C 73.994 12.177 72 10.522 72 8.089 C 72 5.656 74.002 4 76.935 4 C 78.326 4 79.208 4.305 79.779 4.57 L 79.779 5.808 C 78.894 5.415 77.935 5.214 76.967 5.217 C 74.844 5.217 73.403 6.379 73.403 8.089 C 73.403 9.799 74.826 10.972 76.924 10.972 C 77.495 10.972 78.216 10.874 78.658 10.732 L 78.658 8.408 L 79.993 8.408 L 79.993 11.578 C 79.218 11.942 77.97 12.181 76.924 12.181 M 85.16 7.698 C 84.792 7.368 84.385 7.03 84.157 6.808 C 84.157 7.106 84.167 7.586 84.167 7.905 L 84.167 12.038 L 82.791 12.038 L 82.791 4.024 L 82.888 4.024 L 87.844 8.475 L 88.836 9.376 C 88.825 9.071 88.825 8.664 88.825 8.279 L 88.825 4.147 L 90.201 4.147 L 90.201 12.161 L 90.116 12.161 L 85.159 7.698 Z M 42 17.859 L 43.799 14.508 L 43.941 14.508 L 45.743 17.859 L 44.98 17.859 L 44.627 17.224 L 43.107 17.224 L 42.764 17.859 Z M 44.366 16.661 C 44.198 16.331 44.034 16 43.874 15.666 C 43.72 15.993 43.542 16.346 43.378 16.661 Z M 47.799 14.555 C 49.09 14.555 49.85 15.18 49.85 16.207 C 49.85 17.235 49.097 17.859 47.82 17.859 L 46.607 17.859 L 46.607 14.555 Z M 47.32 15.161 L 47.32 17.249 L 47.81 17.249 C 48.63 17.249 49.13 16.868 49.13 16.204 C 49.13 15.539 48.623 15.158 47.791 15.158 L 47.321 15.158 L 47.321 15.161 Z M 52.07 17.907 L 52.087 17.874 L 50.307 14.554 L 51.085 14.554 L 51.795 15.913 C 51.941 16.2 52.059 16.425 52.177 16.672 C 52.341 16.327 52.527 15.986 52.751 15.553 L 53.271 14.558 L 54.05 14.558 L 52.251 17.91 L 52.07 17.91 Z M 55.584 17.859 L 54.87 17.859 L 54.87 14.555 L 55.584 14.555 Z M 56.804 17.739 L 56.726 17.71 L 56.726 17.02 L 56.836 17.068 C 57.146 17.198 57.536 17.286 57.86 17.286 C 58.082 17.286 58.26 17.253 58.381 17.195 C 58.478 17.144 58.535 17.079 58.535 16.988 C 58.535 16.886 58.495 16.81 58.395 16.741 C 58.278 16.657 58.085 16.585 57.793 16.498 C 57.029 16.276 56.697 15.996 56.697 15.459 C 56.697 14.875 57.193 14.5 58.028 14.5 C 58.363 14.5 58.724 14.562 58.984 14.668 L 59.034 14.686 L 59.034 15.357 L 58.924 15.307 C 58.648 15.188 58.35 15.126 58.049 15.125 C 57.839 15.125 57.668 15.155 57.55 15.219 C 57.454 15.27 57.396 15.343 57.396 15.437 C 57.396 15.528 57.436 15.601 57.532 15.673 C 57.65 15.761 57.839 15.84 58.128 15.928 C 58.884 16.156 59.234 16.425 59.234 16.951 C 59.234 17.551 58.742 17.914 57.882 17.914 C 57.514 17.914 57.104 17.844 56.801 17.736 Z M 62.089 14.5 C 63.273 14.5 64.076 15.198 64.076 16.21 C 64.076 17.224 63.27 17.921 62.089 17.921 C 60.908 17.921 60.101 17.224 60.101 16.211 C 60.101 15.198 60.907 14.501 62.088 14.501 Z M 62.089 17.271 C 62.834 17.271 63.352 16.846 63.352 16.211 C 63.352 15.575 62.834 15.147 62.088 15.147 C 61.343 15.147 60.818 15.572 60.818 16.211 C 60.818 16.85 61.339 17.271 62.088 17.271 Z M 66.499 14.558 C 67.373 14.558 67.908 14.954 67.908 15.63 C 67.908 16.073 67.64 16.41 67.188 16.567 L 68.043 17.863 L 67.255 17.863 L 66.505 16.683 L 65.906 16.683 L 65.906 17.863 L 65.2 17.863 L 65.2 14.559 L 66.499 14.559 Z M 65.906 15.165 L 65.906 16.098 L 66.527 16.098 C 66.93 16.098 67.194 15.938 67.194 15.63 C 67.194 15.321 66.924 15.165 66.502 15.165 Z M 69.325 14.591 L 70.263 15.935 L 71.23 14.558 L 72.047 14.558 L 70.62 16.574 L 70.62 17.863 L 69.906 17.863 L 69.906 16.573 L 68.479 14.559 L 69.296 14.559 L 69.321 14.591 Z M 2.034 14.412 L 9.998 14.325 L 11.532 11.558 L 13.58 15.168 L 1.602 15.168 L 1.032 16.17 L 15.285 16.17 L 12.092 10.541 L 12.549 9.717 L 16.673 16.987 L 0.571 16.987 L 0 17.989 L 18.386 17.989 L 13.116 8.7 L 13.559 7.902 L 19.285 18 L 20.42 18 L 10.212 0 Z M 10.212 2.004 L 12.984 6.896 L 12.542 7.695 L 10.305 3.755 L 4.799 13.381 L 3.75 13.392 Z M 10.305 5.752 L 11.981 8.708 L 11.525 9.532 L 10.319 7.408 L 7.139 13.352 L 5.951 13.367 Z M 10.347 9.459 L 10.965 10.545 L 9.423 13.323 L 8.271 13.337 Z M 0 18.002 L 0.57 17 L 16.677 17 L 18.387 18.003 L 0 18.003 Z M 1 16.006 L 1.567 15 L 13.545 15 L 15.254 16.006 Z M 10.078 14.29 L 14.406 6.52 L 13.825 5.5 L 9.5 13.292 Z" fill="transparent" height="18.003px" id="K_8etyHP8" width="90.20100036621093px"><path d="M 1.388 1.232 L 1.388 6.89 L 2.819 6.89 C 5.017 6.89 6.33 5.837 6.33 4.061 C 6.33 2.285 4.996 1.232 2.766 1.232 L 1.387 1.232 Z M 0 8.008 L 0 0.118 L 2.79 0.118 C 5.895 0.118 7.746 1.599 7.746 4.065 C 7.746 6.53 5.916 8.012 2.844 8.012 L 0 8.012 Z M 14.74 5.415 C 14.233 4.438 13.652 3.265 13.166 2.248 C 12.665 3.317 12.137 4.373 11.582 5.415 Z M 13.113 0 L 13.22 0 L 17.53 8.015 L 16.064 8.015 L 15.179 6.413 L 11.129 6.413 L 10.266 8.015 L 8.799 8.015 L 13.109 0 Z M 21.954 1.232 L 21.954 8.008 L 20.567 8.008 L 20.567 1.232 L 17.809 1.232 L 17.809 0.118 L 24.714 0.118 L 24.714 1.232 L 21.955 1.232 Z M 30.927 5.415 C 30.421 4.438 29.84 3.265 29.354 2.248 C 28.853 3.317 28.324 4.373 27.77 5.415 L 30.928 5.415 Z M 29.302 0 L 29.409 0 L 33.719 8.015 L 32.256 8.015 L 31.371 6.413 L 27.321 6.413 L 26.458 8.015 L 24.992 8.015 Z M 35.88 8.008 L 35.88 0.114 L 37.268 0.114 L 37.268 6.89 L 41.158 6.89 L 41.158 8.008 Z" fill="rgb(132, 130, 142)" height="8.015px" id="jAL5eYCXu" transform="translate(24 4)" width="41.15800106811523px"/><path d="M 1.392 0 L 0 0 L 0 7.89 L 1.392 7.89 Z" fill="rgb(132, 130, 142)" height="7.890000000000001px" id="u8cKeOXNI" transform="translate(67.5 4.5)" width="1.391999999999996px"/><path d="M 4.924 8.177 C 1.994 8.177 0 6.522 0 4.089 C 0 1.656 2.002 0 4.935 0 C 6.326 0 7.208 0.305 7.779 0.57 L 7.779 1.808 C 6.894 1.415 5.935 1.214 4.967 1.217 C 2.844 1.217 1.403 2.379 1.403 4.089 C 1.403 5.799 2.826 6.972 4.924 6.972 C 5.495 6.972 6.216 6.874 6.658 6.732 L 6.658 4.408 L 7.993 4.408 L 7.993 7.578 C 7.218 7.942 5.97 8.181 4.924 8.181 M 13.16 3.698 C 12.792 3.368 12.385 3.03 12.157 2.808 C 12.157 3.106 12.167 3.586 12.167 3.905 L 12.167 8.038 L 10.791 8.038 L 10.791 0.024 L 10.888 0.024 L 15.844 4.475 L 16.836 5.376 C 16.825 5.071 16.825 4.664 16.825 4.279 L 16.825 0.147 L 18.201 0.147 L 18.201 8.161 L 18.116 8.161 L 13.159 3.698 Z" fill="rgb(132, 130, 142)" height="8.181px" id="kN7yl8Gfy" transform="translate(72 4)" width="18.201000366210934px"/><path d="M 0 3.359 L 1.799 0.008 L 1.941 0.008 L 3.743 3.359 L 2.98 3.359 L 2.627 2.724 L 1.107 2.724 L 0.764 3.359 Z M 2.366 2.161 C 2.198 1.831 2.034 1.5 1.874 1.166 C 1.72 1.493 1.542 1.846 1.378 2.161 Z M 5.799 0.055 C 7.09 0.055 7.85 0.68 7.85 1.707 C 7.85 2.735 7.097 3.359 5.82 3.359 L 4.607 3.359 L 4.607 0.055 Z M 5.32 0.661 L 5.32 2.749 L 5.81 2.749 C 6.63 2.749 7.13 2.368 7.13 1.704 C 7.13 1.039 6.623 0.658 5.791 0.658 L 5.321 0.658 L 5.321 0.661 Z M 10.07 3.407 L 10.087 3.374 L 8.307 0.054 L 9.085 0.054 L 9.795 1.413 C 9.941 1.7 10.059 1.925 10.177 2.172 C 10.341 1.827 10.527 1.486 10.751 1.053 L 11.271 0.058 L 12.05 0.058 L 10.251 3.41 L 10.07 3.41 Z M 13.584 3.359 L 12.87 3.359 L 12.87 0.055 L 13.584 0.055 Z M 14.804 3.239 L 14.726 3.21 L 14.726 2.52 L 14.836 2.568 C 15.146 2.698 15.536 2.786 15.86 2.786 C 16.082 2.786 16.26 2.753 16.381 2.695 C 16.478 2.644 16.535 2.579 16.535 2.488 C 16.535 2.386 16.495 2.31 16.395 2.241 C 16.278 2.157 16.085 2.085 15.793 1.998 C 15.029 1.776 14.697 1.496 14.697 0.959 C 14.697 0.375 15.193 0 16.028 0 C 16.363 0 16.724 0.062 16.984 0.168 L 17.034 0.186 L 17.034 0.857 L 16.924 0.807 C 16.648 0.688 16.35 0.626 16.049 0.625 C 15.839 0.625 15.668 0.655 15.55 0.719 C 15.454 0.77 15.396 0.843 15.396 0.937 C 15.396 1.028 15.436 1.101 15.532 1.173 C 15.65 1.261 15.839 1.34 16.128 1.428 C 16.884 1.656 17.234 1.925 17.234 2.451 C 17.234 3.051 16.742 3.414 15.882 3.414 C 15.514 3.414 15.104 3.344 14.801 3.236 Z M 20.089 0 C 21.273 0 22.076 0.698 22.076 1.71 C 22.076 2.724 21.27 3.421 20.089 3.421 C 18.908 3.421 18.101 2.724 18.101 1.711 C 18.101 0.698 18.907 0.001 20.088 0.001 Z M 20.089 2.771 C 20.834 2.771 21.352 2.346 21.352 1.711 C 21.352 1.075 20.834 0.647 20.088 0.647 C 19.343 0.647 18.818 1.072 18.818 1.711 C 18.818 2.35 19.339 2.771 20.088 2.771 Z M 24.499 0.058 C 25.373 0.058 25.908 0.454 25.908 1.13 C 25.908 1.573 25.64 1.91 25.188 2.067 L 26.043 3.363 L 25.255 3.363 L 24.505 2.183 L 23.906 2.183 L 23.906 3.363 L 23.2 3.363 L 23.2 0.059 L 24.499 0.059 Z M 23.906 0.665 L 23.906 1.598 L 24.527 1.598 C 24.93 1.598 25.194 1.438 25.194 1.13 C 25.194 0.821 24.924 0.665 24.502 0.665 Z M 27.325 0.091 L 28.263 1.435 L 29.23 0.058 L 30.047 0.058 L 28.62 2.074 L 28.62 3.363 L 27.906 3.363 L 27.906 2.073 L 26.479 0.059 L 27.296 0.059 L 27.321 0.091 Z" fill="rgb(142, 140, 153)" height="3.421000000000001px" id="P22Fbj16y" transform="translate(42 14.5)" width="30.047000091552746px"/><path d="M 2.034 14.412 L 9.998 14.325 L 11.532 11.558 L 13.58 15.168 L 1.602 15.168 L 1.032 16.17 L 15.285 16.17 L 12.092 10.541 L 12.549 9.717 L 16.673 16.987 L 0.571 16.987 L 0 17.989 L 18.386 17.989 L 13.116 8.7 L 13.559 7.902 L 19.285 18 L 20.42 18 L 10.212 0 Z M 10.212 2.004 L 12.984 6.896 L 12.542 7.695 L 10.305 3.755 L 4.799 13.381 L 3.75 13.392 Z M 10.305 5.752 L 11.981 8.708 L 11.525 9.532 L 10.319 7.408 L 7.139 13.352 L 5.951 13.367 Z M 10.347 9.459 L 10.965 10.545 L 9.423 13.323 L 8.271 13.337 Z" fill="url(%23vKxq0SU4w-1921182794-linear-gradient)" height="18px" id="vKxq0SU4w" width="20.42px"/><path d="M 0 1.002 L 0.57 0 L 16.677 0 L 18.387 1.003 L 0 1.003 Z" fill="url(%23qyqFJaVjA-1921182794-linear-gradient)" height="1.0030000000000001px" id="qyqFJaVjA" transform="translate(0 17)" width="18.387px"/><path d="M 0 1.006 L 0.567 0 L 12.545 0 L 14.254 1.006 Z" fill="url(%23KBptSRBQO-1921182794-linear-gradient)" height="1.0060000000000002px" id="KBptSRBQO" transform="translate(1 15)" width="14.254000000000005px"/><path d="M 0.578 8.79 L 4.906 1.02 L 4.325 0 L 0 7.792 Z" fill="url(%23Kgw6PgukY-1921182794-linear-gradient)" height="8.79px" id="Kgw6PgukY" transform="translate(9.5 5.5)" width="4.906000000000006px"/></g></svg>)

The Aligned Perspective

5 min

Read

This guide gives you a practical 7-step checklist covering everything from fiduciary status, to fee structures, conflict disclosures, and values alignment.

Director of Growth

,

Key Takeaways:

Use a 7-step checklist to verify a financial advisor's fiduciary status, understand their fee structure, and ensure their approach aligns with your values and goals.

Request written fiduciary commitments, transparent fee breakdowns, and clear disclosures to protect your interests and avoid conflicts of interest.

Use regulatory tools and ask targeted questions to confidently identify trustworthy, SEC-registered fiduciary advisors. Platforms like Datalign Advisory make the search much simpler.

So, you've decided to hire a financial advisor. Great move. But here's the thing: not all advisors are created equal. Knowing how to evaluate a fiduciary financial advisor is what separates confident, well-protected investors from those who find out too late that their advisor had other priorities.

We've seen it happen. Someone does months of research on index funds and tax-loss harvesting, then hands everything over to an advisor without checking the basics. Verifying credentials, understanding fees, confirming fiduciary status — these steps matter more than most people realize.

This guide gives you a practical 7-step checklist covering everything from fiduciary status, to fee structures, conflict disclosures, and values alignment. And if you'd rather skip the research entirely, Datalign Advisory can match you with a rigorously vetted, SEC-registered fiduciary advisor in minutes.

Step-by-Step Checklist: Verify, Compare Costs, and Confirm Fit

You've already done smart things: maxed out your 401(k), opened a Roth IRA, maybe started building a taxable brokerage account. Now you want someone to help confirm you're on the right track. The problem is, "financial advisor" is a broad term. Anyone can use it. What you actually want is a fiduciary financial advisor — someone legally required to act in your best interest.

Here's how to evaluate a fiduciary financial advisor using three core checkpoints.

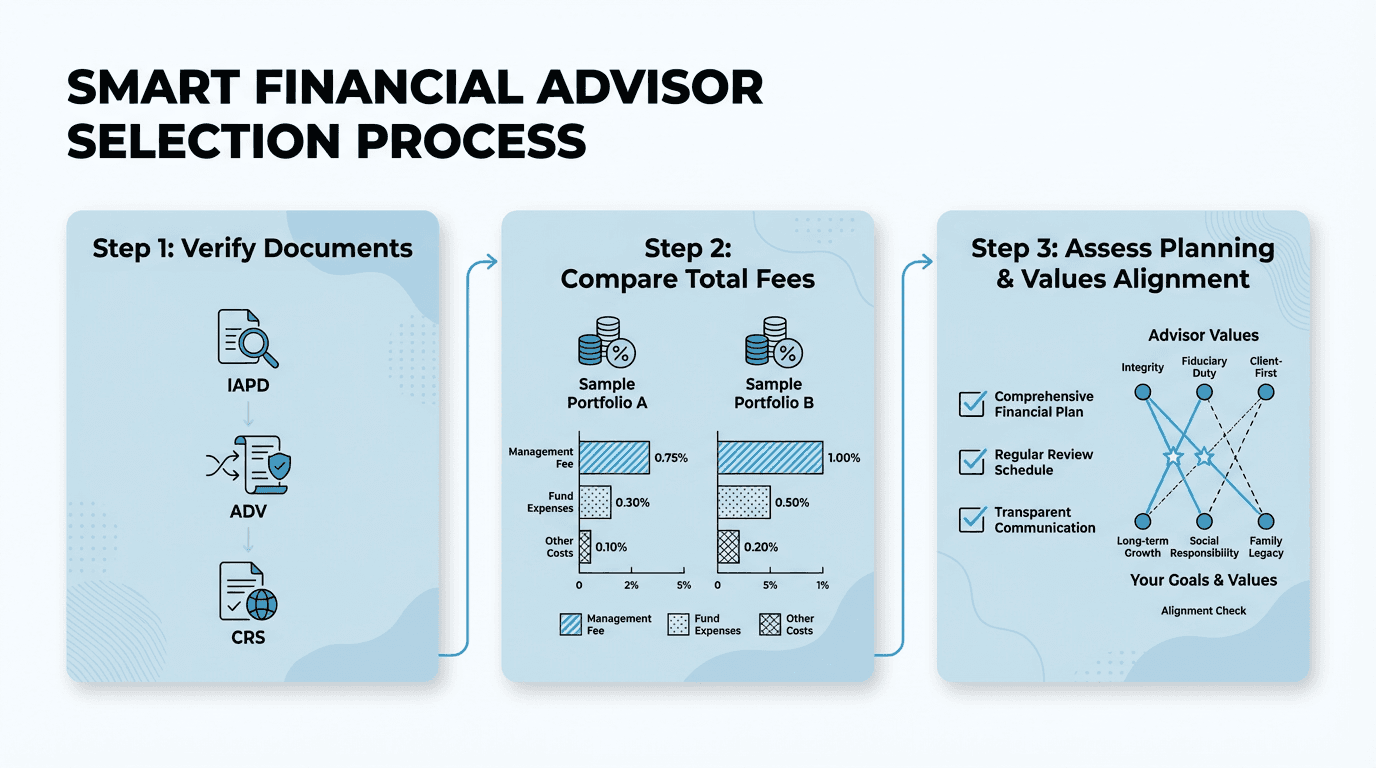

Verify Registration and Get Written Commitments

Start with the SEC's IAPD database. Search the firm and advisor by name. From there, download their Form ADV (it covers services, fees, and conflicts of interest) and their Form CRS (a plain-language summary of the relationship and costs).

Once you've reviewed those documents, request a written fiduciary commitment. This should cover all of your accounts, not just advisory ones. A verbal promise is easy to walk back. A written commitment is enforceable. Advisor credentials matter, and verifying them upfront protects you down the road.

Calculate Your Total Annual Costs

Ask for a one-page fee breakdown. It should show your total annual cost on both your current portfolio value and your expected end-of-year balance. Advisory fees, fund expenses, trading costs, planning charges: all of it.

Most people only ask about the advisory fee percentage. That's a mistake. The full picture often looks quite different. Understanding how advisors are compensated before you sign anything can prevent unpleasant surprises later.

Assess Philosophy and Values Alignment

This step is often skipped, which is why so many people end up in advisor relationships that technically work but never feel quite right. Review their investment approach, how often they meet with clients, and their conflict management policies.

Ask for a sample financial plan and a proposed service calendar for your first year. Then ask specifically: how do they incorporate your values — sustainability, family priorities, community focus — into their recommendations? A good fiduciary advisor doesn't just manage a portfolio. They align their approach to your life. This kind of comprehensive evaluation is what confirms you've found a long-term fit.

What Questions Should I Ask a Fiduciary Financial Advisor Before Hiring?

Good questions reveal things that polished advisor bios don't. Here are the seven we recommend asking before committing to anyone.

Will you provide a written fiduciary commitment for all advice you give me? Ask for Form ADV Parts 2A and 2B, Form CRS, and a signed letter confirming fiduciary duty applies to every recommendation, not just investment accounts.

What will I pay in total fees this year, broken down line by line? Get a one-page illustration showing advisory fees, fund expenses, trading costs, and planning charges tied to your actual expected portfolio size.

How are you compensated, and do you receive payments from product companies? Find out whether they're fee-only or fee-based, and ask specifically about revenue sharing arrangements with mutual fund companies, insurance companies, or other providers.

What does your onboarding process look like in the first 35 days? A clear, structured onboarding timeline shows the advisor is organized and client-focused, not just gathering assets.

Can you show me a sample financial plan similar to what you'd create for me? This reveals whether they offer comprehensive planning or primarily manage investments. Know which one you're hiring.

How will you incorporate my values and family priorities into my financial strategy? Ask for specific examples: clients who support extended family, pursue sustainable investing, or have culturally specific planning needs.

What's your investment philosophy, and how do you handle market downturns? Look for a clear, consistent framework. How an advisor responds to volatility tells you far more than how they handle gains.

FAQs About Evaluating a Fiduciary Financial Advisor

These questions come up constantly, especially from people who are new to working with advisors. Here are straight answers.

Where do I officially verify an advisor's fiduciary registration?

Start with the SEC's IAPD database. It confirms registration and gives you access to disclosure documents. Form ADV reveals business practices and conflicts of interest. Form CRS summarizes services in plain language. You can also check disciplinary history and firm background there. Request a written fiduciary commitment covering all advice as a final step.

What red flags should I look out for when evaluating a fiduciary financial advisor?

Vague fee explanations are a big one. So is any reluctance to share regulatory filings. Watch out for pressure to buy proprietary products, sales quotas, commission incentives, or revenue-sharing arrangements. If an advisor avoids putting their fiduciary duty in writing or can't clearly explain how they're paid, those are serious warning signs.

What's the difference between fee-only and fee-based advisors?

Fee-only advisors are compensated entirely by client fees. No commissions, no outside payments. Fee-based advisors may earn both client advisory fees and commissions from product sales. Ask directly when commissions apply and how potential and known conflicts of interest are managed. Fee-only advisors tend to have cleaner alignment with your interests, though some fee-based advisors maintain strong fiduciary standards through proper disclosure.

How can I find an advisor who understands my values and background?

Ask potential advisors directly about their experience with clients from diverse backgrounds. How do they incorporate personal values into planning? Can they walk you through how they've helped clients balance family support with wealth building? Look for advisors with relevant credentials and ask specifically about their approach to sustainable investing or culturally sensitive financial strategies.

Should I get the fiduciary commitment in writing?

Absolutely. A verbal fiduciary promise is almost meaningless when a conflict actually arises. The written document should state that the advisor will always act in your best interest, disclose all conflicts, and provide suitable recommendations across all services. That commitment becomes part of your service agreement and gives you real protection.

Find a Trusted, Vetted Fiduciary — Matched to You

Knowing how to evaluate a fiduciary financial advisor doesn't have to be complicated. You now have the checklist: verify SEC registration, decode fee structures, get commitments in writing, and confirm genuine values alignment. These steps work.

Armed with the right questions, you can walk into any advisor meeting with clarity and confidence. The verification process we've laid out protects your interests from day one.

Want to skip the research entirely? Datalign Advisory's free matching platform can connect you in minutes with a rigorously vetted, SEC-registered fiduciary advisor. Our AI-enhanced matching draws from a network that includes 86% of Barron's Top 100 advisors. You'll move forward with both clarity and confidence.

Disclaimer: This information is for educational purposes only and is not intended as, nor should it be relied upon as, individualized financial, investment, tax, or legal advice, and you should consult a qualified professional about your specific circumstances before making any financial decisions.